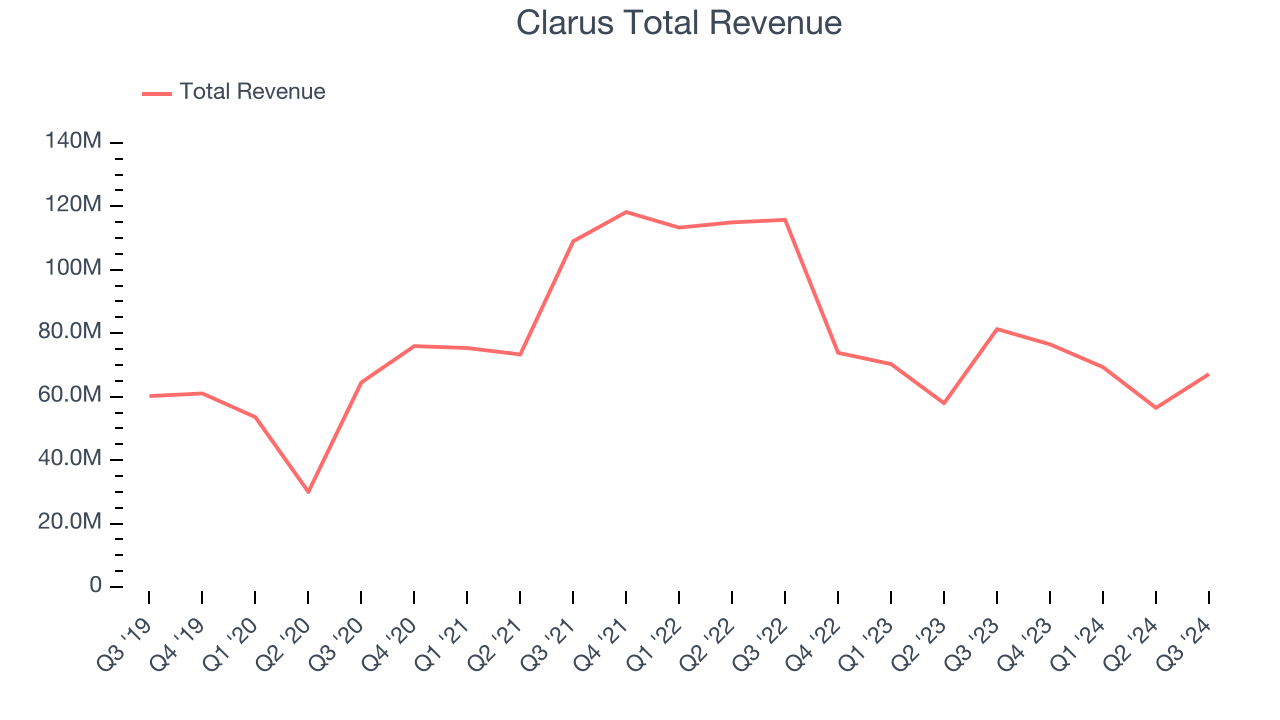

Outdoor lifestyle and equipment company Clarus (NASDAQ:CLAR) fell short of the market’s revenue expectations in Q3 CY2024, with sales falling 17.4% year on year to $67.12 million. The company’s full-year revenue guidance of $263 million at the midpoint came in 4.3% below analysts’ estimates. Its non-GAAP profit of $0.05 per share was also 37.5% below analysts’ consensus estimates.

Is now the time to buy Clarus? Find out by accessing our full research report, it’s free.

Clarus (CLAR) Q3 CY2024 Highlights:

- Revenue: $67.12 million vs analyst estimates of $73.01 million (8.1% miss)

- Adjusted EPS: $0.05 vs analyst expectations of $0.08 (37.5% miss)

- EBITDA: $2.44 million vs analyst estimates of $4.27 million (42.9% miss)

- The company dropped its revenue guidance for the full year to $263 million at the midpoint from $275 million, a 4.4% decrease

- EBITDA guidance for the full year is $8 million at the midpoint, below analyst estimates of $11.21 million

- Gross Margin (GAAP): 35%, up from 20.6% in the same quarter last year

- Operating Margin: -8%, down from -3.9% in the same quarter last year

- EBITDA Margin: 3.6%, in line with the same quarter last year

- Market Capitalization: $185.3 million

Management Commentary“While macroeconomic headwinds have continued to limit consumer demand in the near-term, our focus in the third quarter was on advancing our strategic plan to position Clarus for long-term profitable growth,” said Warren Kanders, Clarus’ Executive Chairman.

Company Overview

Initially a financial services business, Clarus (NASDAQ:CLAR) designs, manufactures, and distributes outdoor equipment and lifestyle products.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Sales Growth

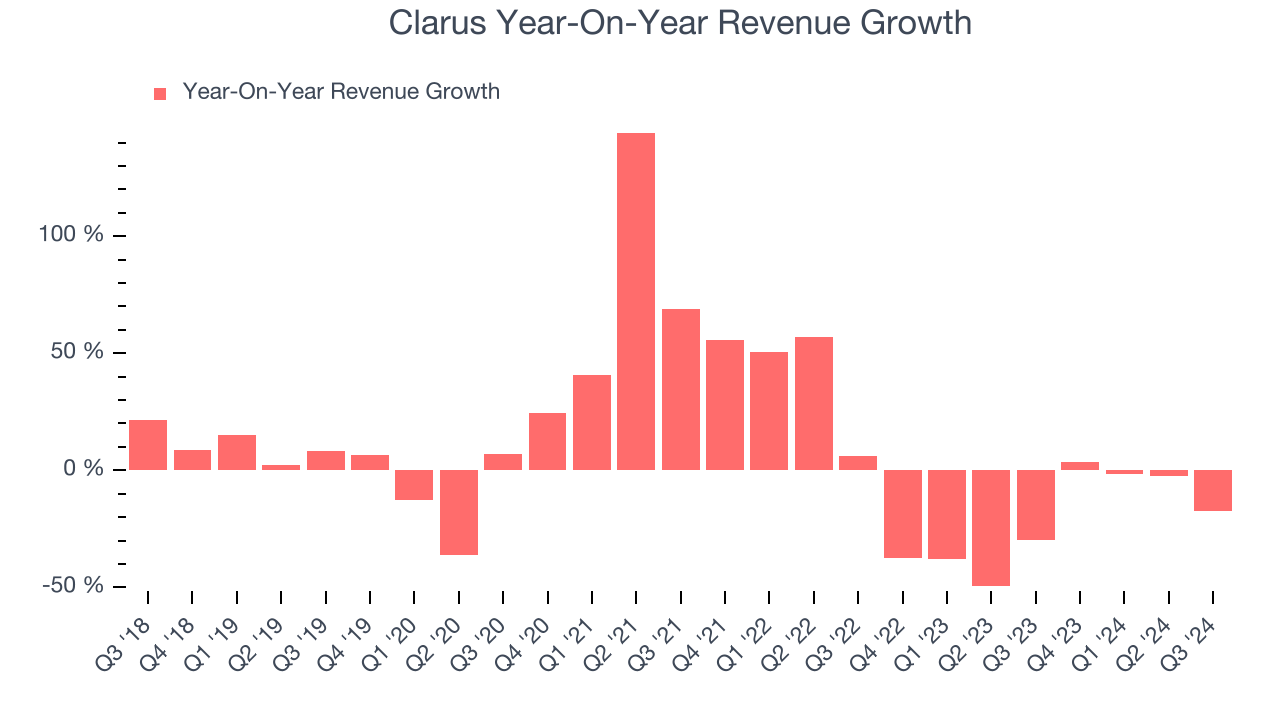

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Clarus grew its sales at a sluggish 3.6% compounded annual growth rate. This shows it failed to expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Clarus’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 23.6% annually.

This quarter, Clarus missed Wall Street’s estimates and reported a rather uninspiring 17.4% year-on-year revenue decline, generating $67.12 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 10.3% over the next 12 months, an improvement versus the last two years. While this projection illustrates the market thinks its newer products and services will spur better performance, it is still below average for the sector.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

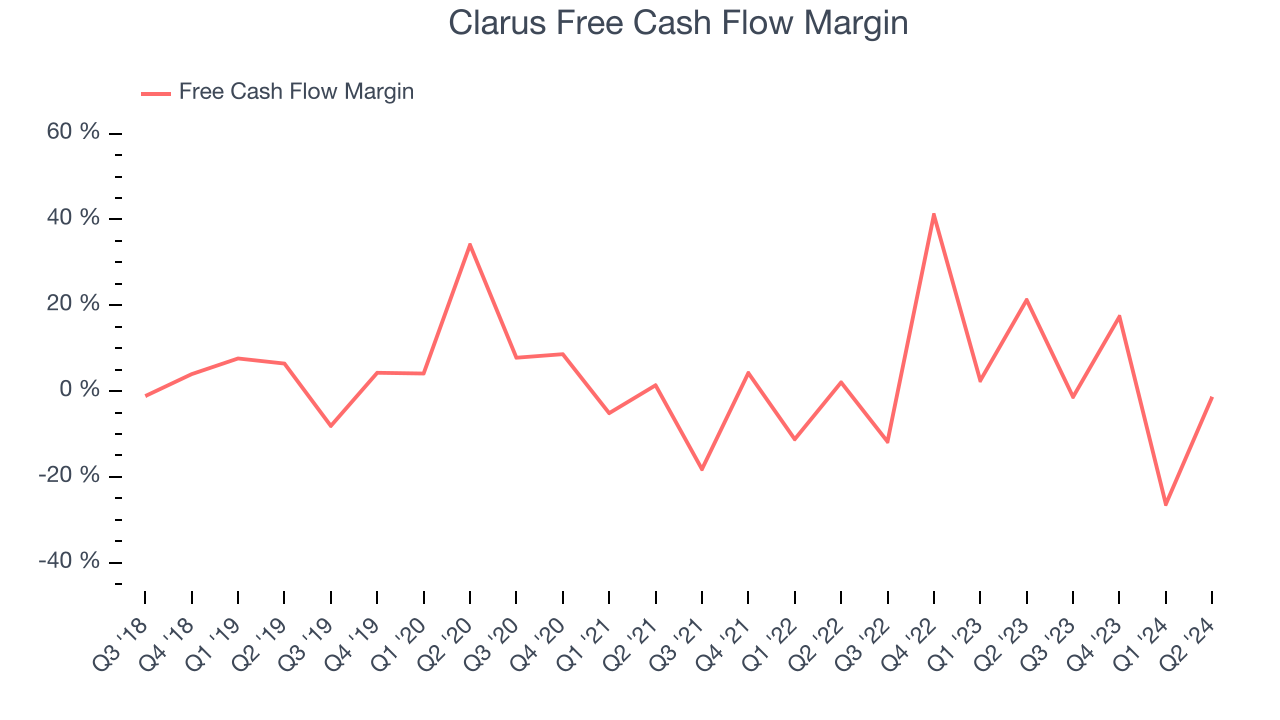

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Clarus has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 7.7%, subpar for a consumer discretionary business.

The company’s cash burn increased from $1.10 million of lost cash in the same quarter last year . These numbers deviate from its longer-term margin, raising some eyebrows.

Key Takeaways from Clarus’s Q3 Results

We struggled to find many strong positives in these results. Its full-year revenue guidance missed and its EBITDA guidance for the full year fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $4.75 immediately after reporting.

Is Clarus an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.