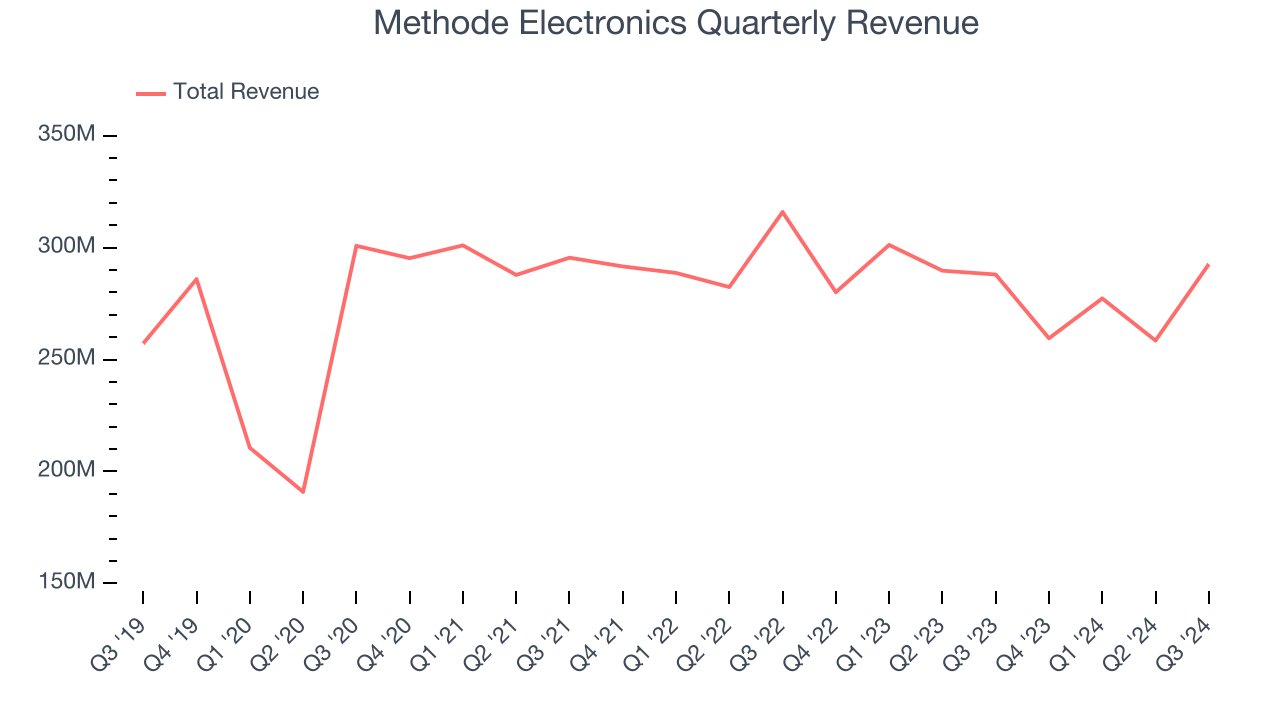

Custom-engineered solutions manufacturer Methode Electronics (NYSE:MEI) reported Q3 CY2024 results topping the market’s revenue expectations, with sales up 1.6% year on year to $292.6 million. Its non-GAAP profit of $0.14 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Methode Electronics? Find out by accessing our full research report, it’s free.

Methode Electronics (MEI) Q3 CY2024 Highlights:

- Revenue: $292.6 million vs analyst estimates of $268.5 million (1.6% year-on-year growth, 9% beat)

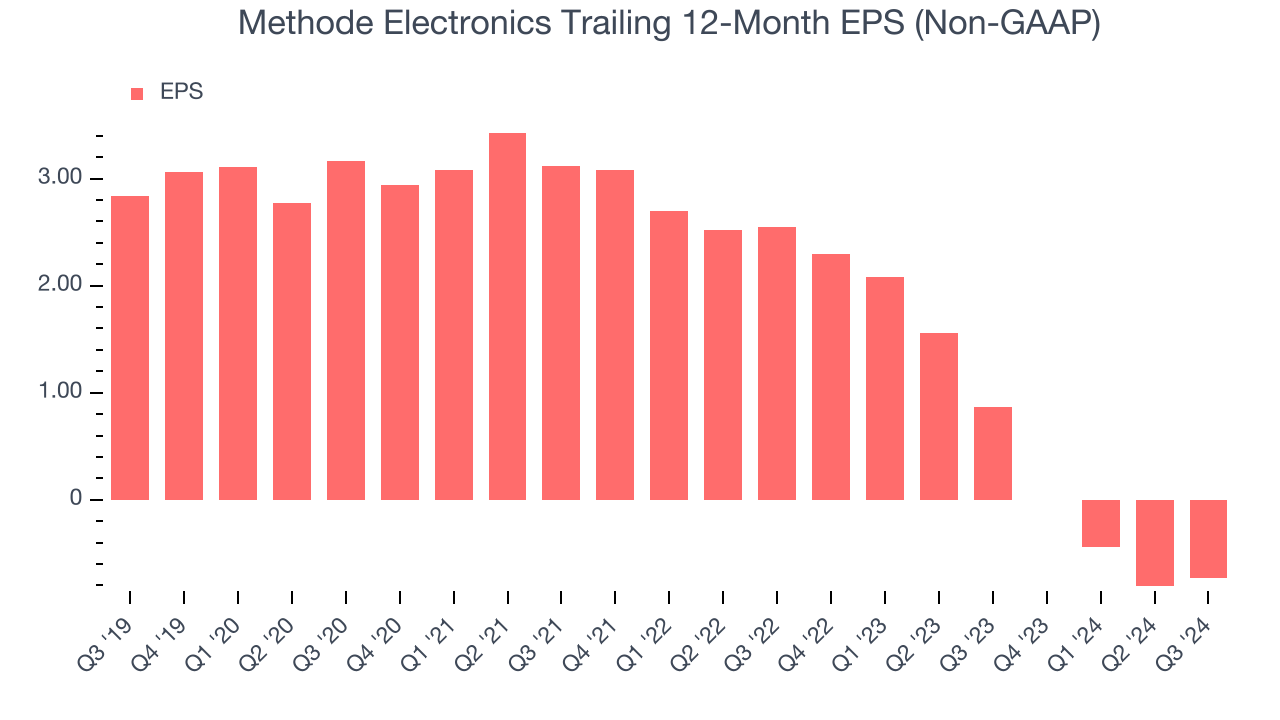

- Adjusted EPS: $0.14 vs analyst estimates of -$0.16 (significant beat)

- Adjusted EBITDA: $26.7 million vs analyst estimates of $13.44 million (9.1% margin, 98.6% beat)

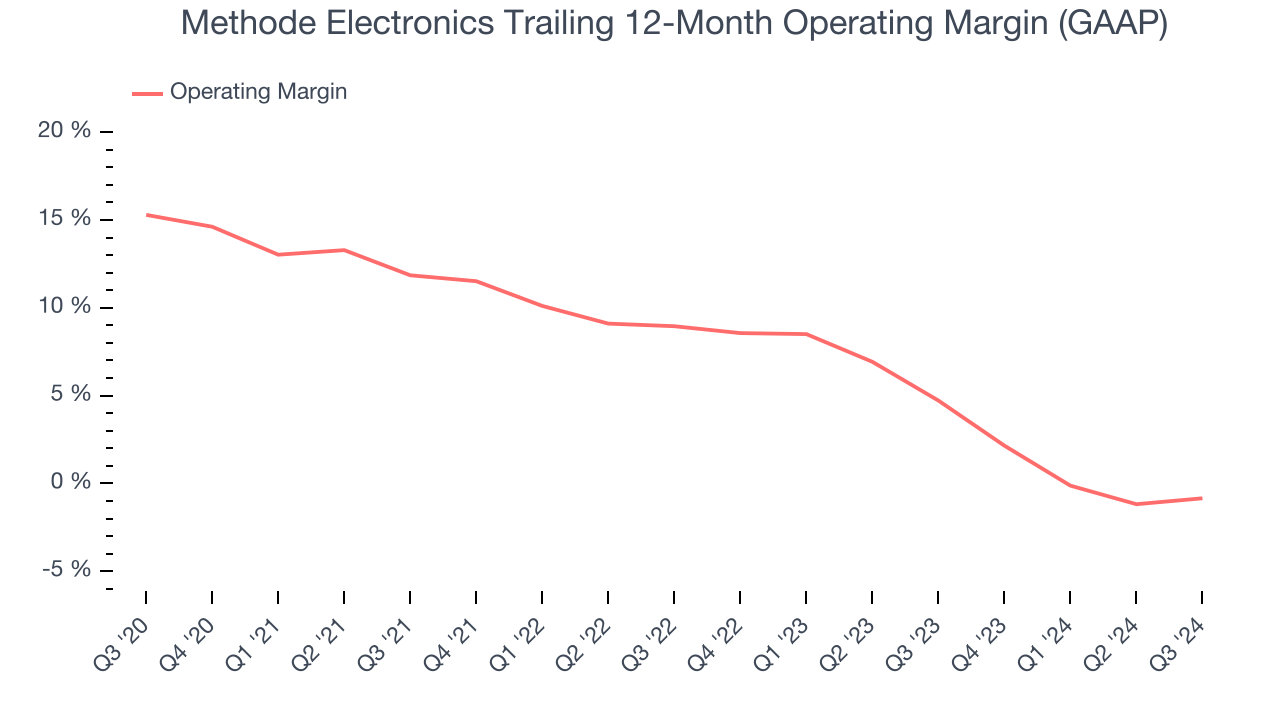

- Operating Margin: 3.2%, up from 2% in the same quarter last year

- Free Cash Flow was -$58.4 million compared to -$11.3 million in the same quarter last year

- Market Capitalization: $409.2 million

Management CommentsPresident and Chief Executive Officer Jon DeGaynor said, “The team is energized, and these results demonstrate that we are heading in the right direction. Our sales in the quarter were the highest that we have reported since fiscal 2023, and our pre-tax income returned to positive territory. Our bookings remained solid, and our EV sales activity is steadily growing.”

Company Overview

Founded in 1946, Methode Electronics (NYSE:MEI) is a global supplier of custom-engineered solutions for Original Equipment Manufacturers (OEMs).

Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Methode Electronics struggled to consistently increase demand as its $1.09 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Methode Electronics’s recent history shows its demand has stayed suppressed as its revenue has declined by 3.9% annually over the last two years.

This quarter, Methode Electronics reported modest year-on-year revenue growth of 1.6% but beat Wall Street’s estimates by 9%.

Looking ahead, sell-side analysts expect revenue to grow 2.5% over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Methode Electronics was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.9% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Methode Electronics’s operating margin decreased by 16.1 percentage points over the last five years. The company’s performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn’t pass those costs onto its customers.

In Q3, Methode Electronics generated an operating profit margin of 3.2%, up 1.2 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Methode Electronics, its EPS declined by 17.7% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

Diving into the nuances of Methode Electronics’s earnings can give us a better understanding of its performance. As we mentioned earlier, Methode Electronics’s operating margin improved this quarter but declined by 16.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business. For Methode Electronics, its two-year annual EPS declines of 51.2% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q3, Methode Electronics reported EPS at $0.14, up from $0.06 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast Methode Electronics’s full-year EPS of negative $0.73 will reach break even.

Key Takeaways from Methode Electronics’s Q3 Results

We were impressed by how significantly Methode Electronics blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. Zooming out, we think this quarter featured some important positives. The stock traded up 18.2% to $13.74 immediately following the results.

Methode Electronics may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.