Online advertising giant Alphabet (NASDAQ:GOOGL) beat Wall Street’s revenue expectations in Q3 CY2024, with sales up 15.1% year on year to $88.27 billion. Its EPS of $2.12 per share was also 14.8% above analysts’ consensus estimates.

Is now the time to buy Alphabet? Find out by accessing our full research report, it’s free.

Alphabet (GOOGL) Q3 CY2024 Highlights:

- Revenue: $88.27 billion vs analyst estimates of $86.22 billion (2.4% beat)

- Operating Profit (GAAP): $28.52 billion vs analyst estimates of $26.69 billion (6.9% beat)

- EPS (GAAP): $2.12 vs analyst estimates of $1.85 (14.8% beat)

- Google Search Revenue: $49.39 billion vs analyst estimates of $49.15 billion (small beat)

- Google Cloud Revenue: $11.35 billion vs analyst estimates of $10.87 billion (4.5% beat)

- YouTube Revenue: $8.92 billion vs analyst estimates of $8.87 billion (small beat)

- Google Services Operating Profit: $30.86 billion vs analyst estimates of $28.64 billion (7.7% beat)

- Google Cloud Operating Profit: $1.95 billion vs analyst estimates of $1.12 billion (73.4% beat)

- Operating Margin: 32.3%, up from 27.8% in the same quarter last year

- Free Cash Flow Margin: 20%, down from 29.5% in the same quarter last year

- Market Capitalization: $2.06 trillion

Key Topics & Areas Of Debate

AI is likely the hottest topic in the world of investing today. Regarding Alphabet, the debate is about how AI’s advancement will impact the company’s bread-and-butter Search business. It is a business where Alphabet has dominant market share, and it is also highly profitable.

Will the development of AI hurt Alphabet because OpenAI’s ChatGPT and even Microsoft’s Bing will take market share from Google, once thought to be nearly invincible in the online search market? Or will Alphabet’s Gemini product, first announced in December 2023, allow the company to dominate the Search market for years or even decades to come given its brand recognition?

As background, Gemini is designed to advance natural language understanding and meet certain thresholds in conversational and contextual understanding. In short, it is meant to provide even more accurate and personalized results, which would be a replay of what made Google so successful decades ago.

Despite its scale and dominance, Alphabet doesn’t operate in a vacuum. ChatGPT and Microsoft’s (NASDAQ:MSFT) new and improved Bing engine are current competitors to Google Search while Meta (NASDAQ:META) is extending beyond social media and into the online search market with its AI-powered assistant.

Alphabet runs into Microsoft often, as it is also one of its primary adversaries in the public cloud services market along with Amazon’s formidable AWS (NASDAQ:AMZN). Finally, Netflix (NASDAQ:NFLX), Disney (NYSE:DIS), and many other video streaming platforms go head-to-head against the company’s YouTube segment.

Revenue Growth

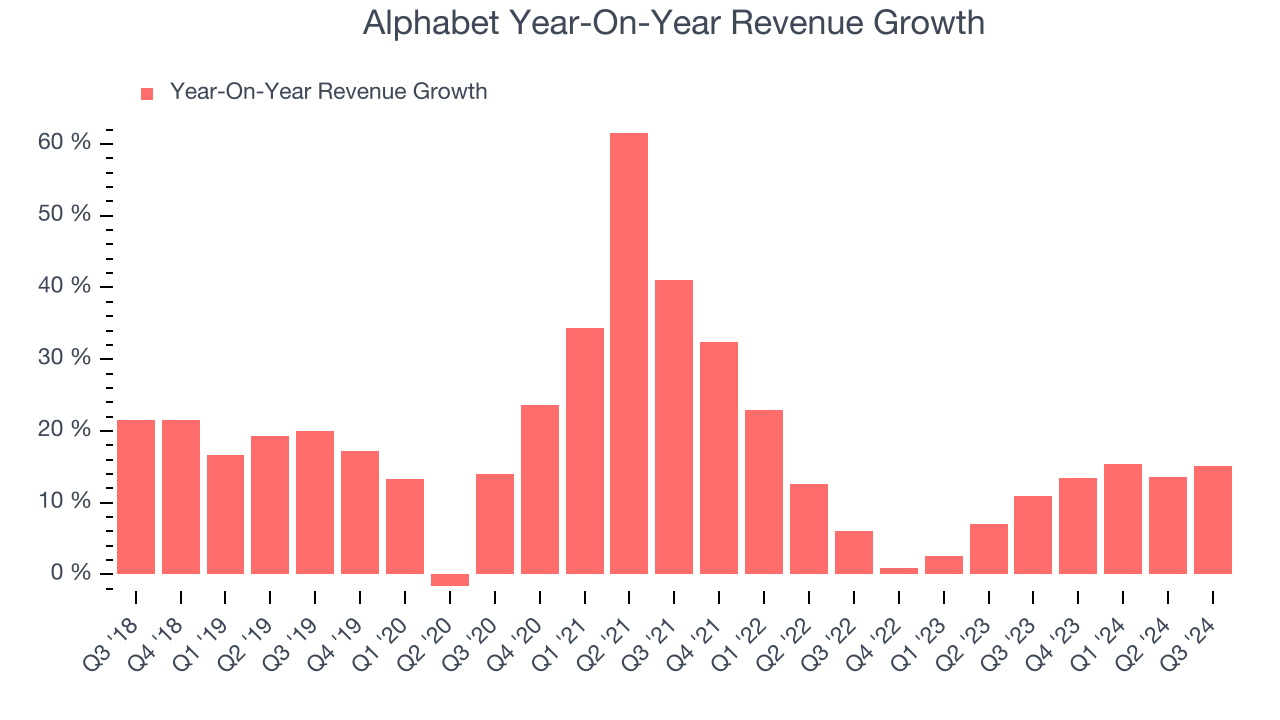

Alphabet proves that huge, scaled companies can still grow quickly. The company’s revenue base of $155.1 billion five years ago has more than doubled to $339.9 billion in the last year, translating into an incredible 17% annualized growth rate.

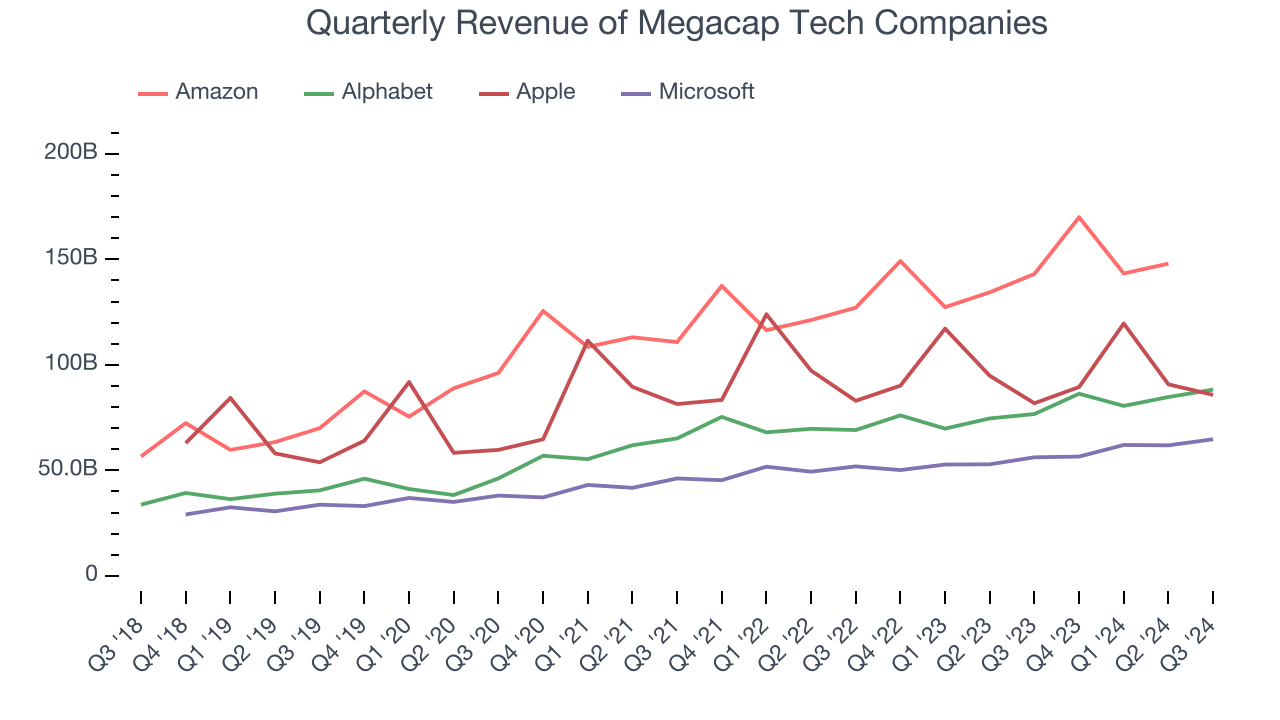

Alphabet’s growth over the same period was also higher than its megacap peers, Amazon (19.1%), Microsoft (14.3%), and Apple (8.3%). Comparing the four is relevant because investors often pit them against each other to derive their valuations. With these benchmarks in mind, we think Alphabet’s price is attractive.

Long-term growth reigns supreme in fundamentals, but for megacap tech companies, a half-decade historical view may miss emerging trends like AI. Alphabet’s annualized revenue growth of 9.8% over the last two years is below its five-year trend, but we still think the results were good and suggest demand was strong.

This quarter, Alphabet reported year-on-year revenue growth of 15.1%, and its $88.27 billion of revenue exceeded Wall Street’s estimates by 2.4%. Looking ahead, sell-side analysts expect revenue to grow 10.6% over the next 12 months, similar to its two-year rate. This projection is healthy for a company of its scale and illustrates the market sees some success for its AI-enabling products.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Google Search: Alphabet’s Bread-and-Butter

The most topical question surrounding Alphabet today is: “Will new Generative-AI products like ChatGPT disrupt Google Search and its 80%+ market share?”.

We can gain further insight by comparing Google Search to Meta and Microsoft’s Bing. Meta is Alphabet’s equivalent in social media advertising and is creeping into search with Meta AI, powered by the Llama large language model. Bing is a more direct competitor and benefits from its integration with ChatGPT through Microsoft’s partnership with OpenAI, though it is the distant number two player.

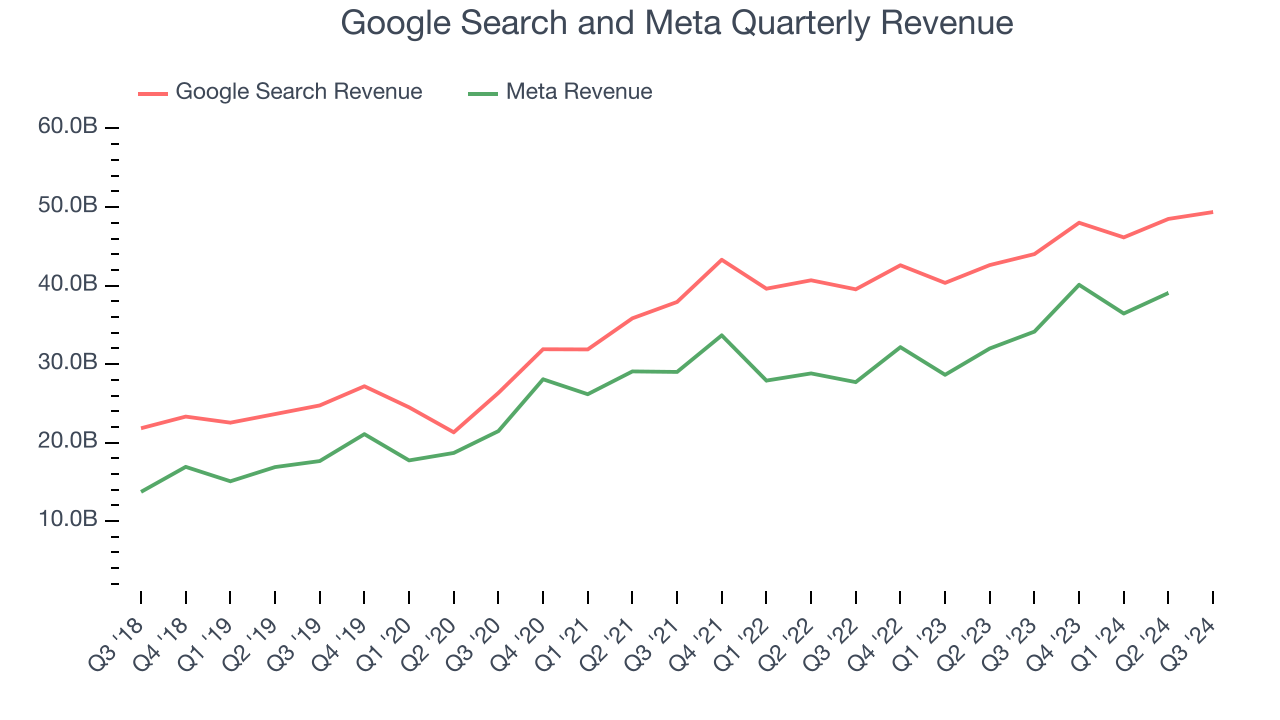

Google Search is by far the most considerable portion of Alphabet’s revenue at 56.5%, and it grew at a 15.3% annualized rate over the last five years, slower than total revenue. The previous two years also saw deceleration as it grew 8.5% annually.

When looking across the competitive landscape, its two-year result was lower than Meta’s 12%. This shows digital advertising dollars could be flowing to social media because of Meta’s improved AI algorithms and targeting capabilities. Alphabet bulls would argue this trend could reverse because the return on investment from keyword-driven advertising is more tangible, but that hasn’t been the case lately.

Quarterly performance is particularly relevant for Alphabet because it captures the growth of AI and signals whether investors are overestimating its competitive impact. Google Search revenue met Wall Street’s consensus estimates in Q3 and recorded a year-on-year increase of 12.2%.

While this was slower than Bing’s 16%, it’s important to consider that Bing is starting from a much smaller revenue base and doesn’t pose a significant threat yet. Still, Alphabet must either start topping Google Search projections or outperform in other segments like Google Cloud Platform and YouTube to satisfy Wall Street.

Key Takeaways from Alphabet’s Q3 Results

We enjoyed seeing Alphabet exceed analysts’ revenue, operating income, and EPS expectations this quarter. The segments themselves were also all solid, with Search, YouTube, and Cloud all exceeding revenue estimates. Operating profit at the segments also beat. Guidance will be provided on the call, which could further move the stock. Zooming out, we think this quarter was quite good. The stock traded up 3.7% to $176 immediately following the results.

Alphabet may have had a good quarter, but does that mean you should invest right now?When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.