Energy Recovery has had an impressive run over the past six months as its shares have beaten the S&P 500 by 13.2%. The stock now trades at $16.11, marking a 23.6% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is it too late to buy ERII? Find out in our full research report, it’s free.

Why Is Energy Recovery a Good Business?

Having saved far more than a trillion gallons of water, Energy Recovery (NASDAQ:ERII) provides energy recovery devices to the water treatment, oil and gas, and chemical processing sectors.

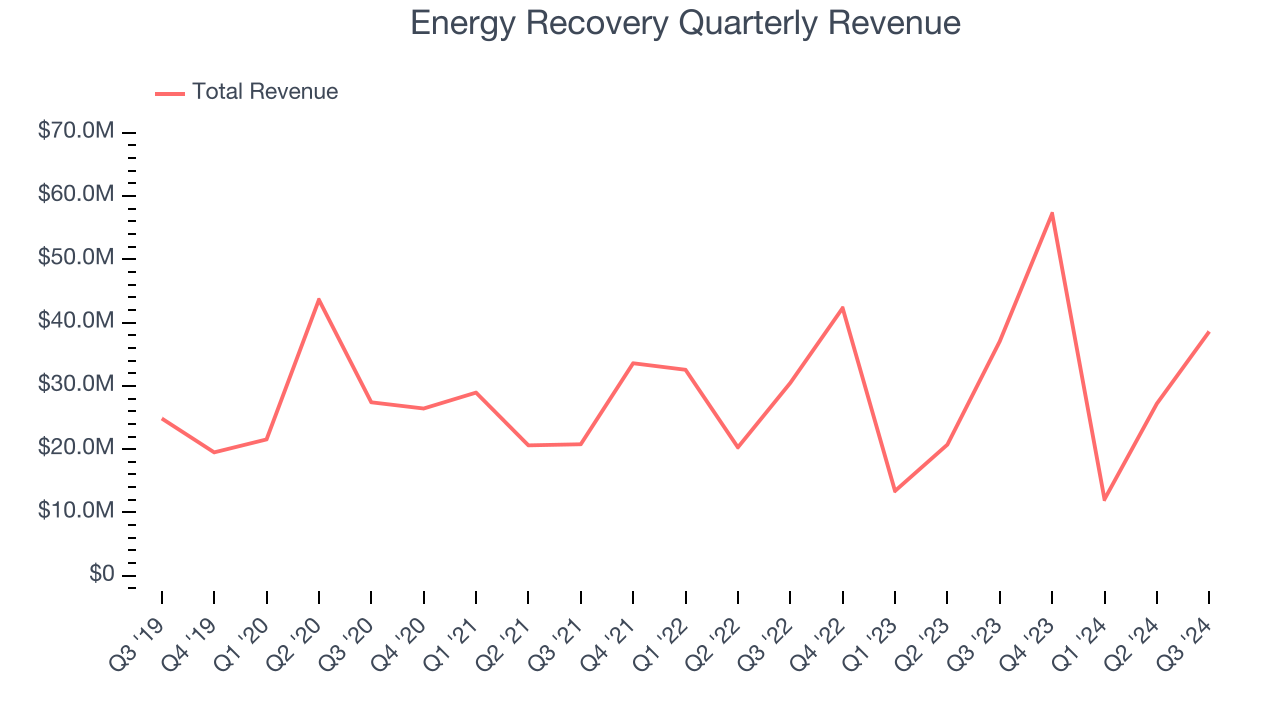

1. Long-Term Revenue Growth Shows Strong Momentum

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Energy Recovery grew its sales at a solid 9.7% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers.

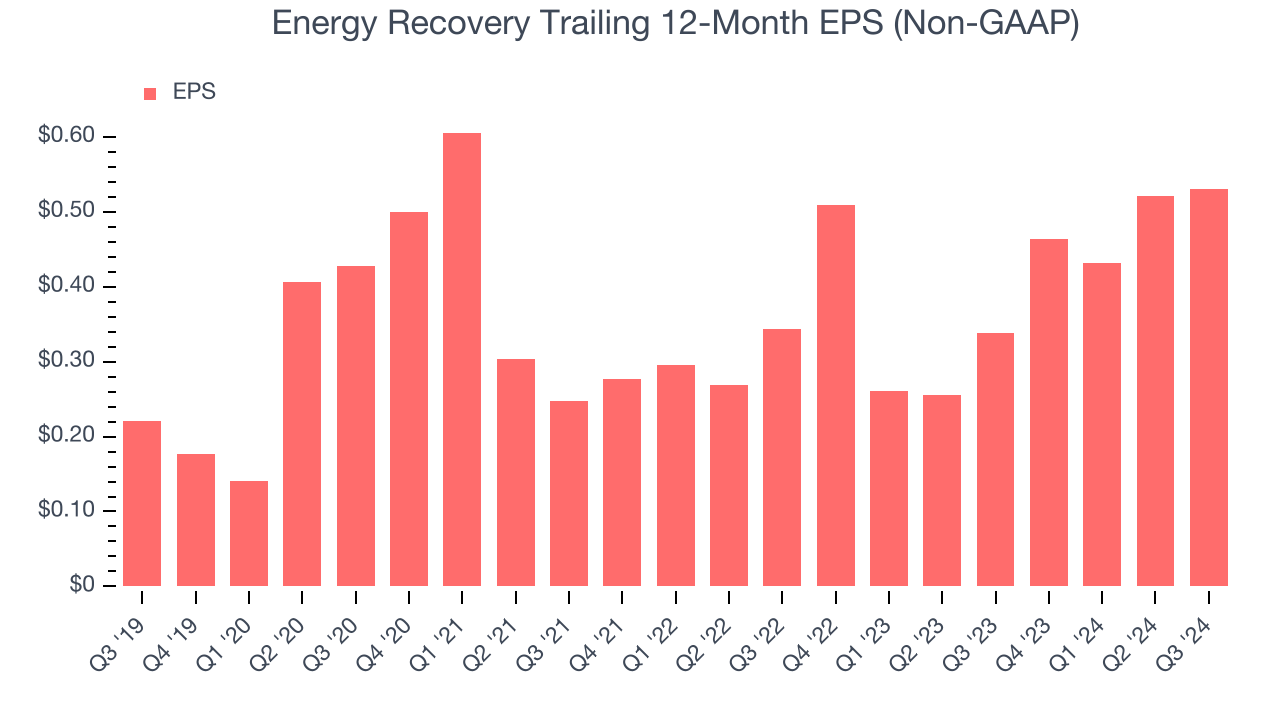

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Energy Recovery’s EPS grew at an astounding 19.2% compounded annual growth rate over the last five years, higher than its 9.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

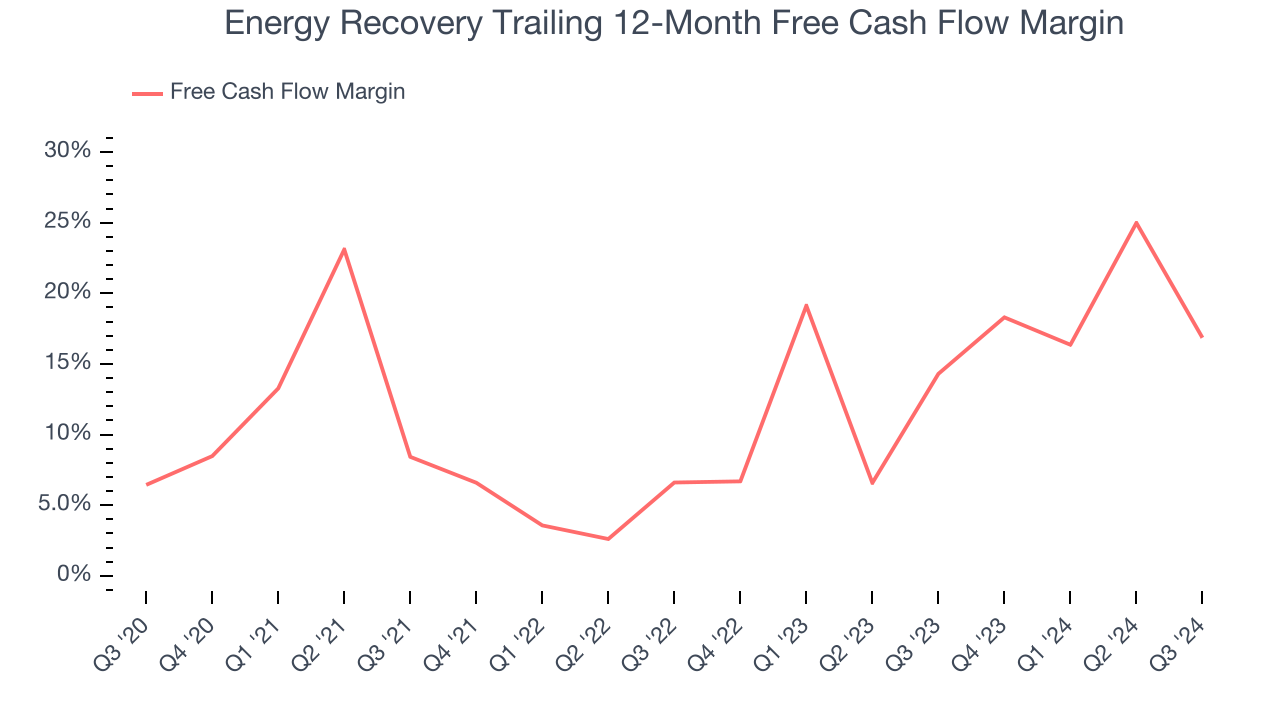

3. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Energy Recovery’s margin expanded by 10.4 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose by more than its operating profitability. Energy Recovery’s free cash flow margin for the trailing 12 months was 16.9%.

Final Judgment

These are just a few reasons Energy Recovery is a rock-solid business worth owning, and with its shares topping the market in recent months, the stock trades at 23× forward price-to-earnings (or $16.11 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Energy Recovery

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.