The Bergey Excel 15 wind turbine, developed through CIP, has reduced the cost of energy by 50% compared to the Bergey Excel 10 wind turbine. Photo from Jordan Nelson, Nelson Aerial Productions

The Bergey Excel 15 wind turbine, developed through CIP, has reduced the cost of energy by 50% compared to the Bergey Excel 10 wind turbine. Photo from Jordan Nelson, Nelson Aerial Productions The U.S. has the potential to profitably provide nearly 1,400 GW of distributed wind energy capacity today, according to new analysis from the National Renewable Energy Laboratory.

NREL researchers set out to analyze the role that distributed wind energy could play in reaching the U.S. goal of 100% clean electricity by 2035. They determined that the U.S. has enough distributed wind energy potential to supply more than half of current U.S. annual electricity consumption.

But the right conditions must exist to realize the opportunities for distributed wind, NREL notes.

Distributed wind energy refers to wind technologies deployed as distributed energy resources. These technologies are place-based solutions that support individuals, communities, and businesses transitioning to carbon-free electricity.

Distributed wind can be placed in behind-the-meter applications, where the system directly offsets a specific end user’s consumption of retail electricity supply, or in front-of-the-meter applications where the system is interconnected to the distribution network and provides community-scale energy supply while bolstering the robustness, reliability, and resiliency of the local distribution network.

Distributed wind installations can range from a less-than-1-kilowatt off-grid wind turbine that powers telecommunications equipment to a 10 MW community-scale energy facility.

From 2003 through 2020, over 87,000 wind turbines were deployed in distributed applications across all 50 states, Puerto Rico, the U.S. Virgin Islands, and Guam, totaling 1,055 MW in cumulative capacity. Iowa, Minnesota, Massachusetts, California, and Texas lead the country with the most distributed wind capacity currently installed.

To determine the potential for distributed wind energy in the U.S., NREL used modeling that included real-world dimensions from a data set of 150 million parcels of property. The 2022 study, which builds on previous research in 2016, was improved to consider front-of-the-meter wind systems, in addition to behind-the-meter applications.

“Our study is one of the first demonstrations of parcel-level distributed energy resources analysis and advances wind economic and technical potential assessments with unprecedented resolution,” said Kevin McCabe, NREL analyst and a developer of the modeling platform. “With this new level of detail, we can identify trends by land-use type, end-use sector, and geography.”

A megawatt-class turbine in a behind-the-meter distributed wind application. Photo by Hank Doster, One Energy Enterprises LLC

A megawatt-class turbine in a behind-the-meter distributed wind application. Photo by Hank Doster, One Energy Enterprises LLCNREL found that U.S. distributed wind has abundant economic potential, or the potential that would have a positive return on investment. Entire regions of the country could profitably provide hundreds of gigawatts today if deployed. In 2035, terawatts of capacity could be possible.

NREL examined three primary factors that it said could help unlock distributed wind’s potential:

- Improved financing and performance to reduce the cost of wind energy

- Relaxed siting restrictions to open up more available land for wind development—a previous NREL study revealed a 7X difference in total U.S. wind technical potential in 2050 between the least and most restrictive siting restrictions

- An investment tax credit renewal and net metering. Currently, customers can receive a 26% tax credit for qualifying wind turbines below 100 kilowatts and solar panels installed between 2020 and 2022. The tax credit will expire in 2024 unless Congress renews it. Net metering is a metering and billing arrangement where distributed energy generation system owners are compensated for any generation that is not used and exported to the utility grid.

Under the most optimistic conditions—including aggressive cost declines, more relaxed siting constraints than today, and strategic extension and expansion of current tax credits and policies—NREL found that front-of-the-meter wind could provide over 4,000 gigawatts of capacity and behind-the-meter wind could provide over 1,700 GW of capacity in 2035.

In the least optimistic conditions, front-of-the-meter wind capacity was found to decrease to 42 GW and behind-the-meter wind capacity to 440 GW in 2035.

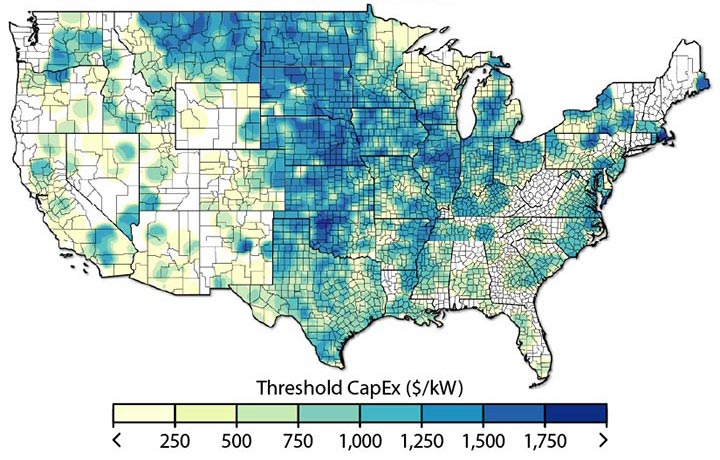

Front-of-the-meter wind – Baseline 2022 scenario The economic potential of front-of-the-meter wind applications in 2022. Oklahoma, Nebraska, Illinois, Kansas, Iowa, South Dakota, Pennsylvania, New York, Montana, and New Mexico have the highest potential.Behind-the-meter wind – Baseline 2022 scenario

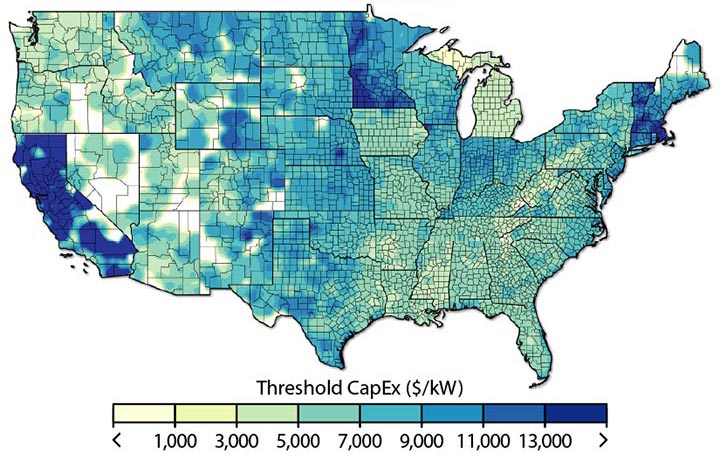

The economic potential of front-of-the-meter wind applications in 2022. Oklahoma, Nebraska, Illinois, Kansas, Iowa, South Dakota, Pennsylvania, New York, Montana, and New Mexico have the highest potential.Behind-the-meter wind – Baseline 2022 scenario The economic potential of behind-the-meter wind applications in 2022. Texas, Minnesota, Montana, Colorado, Oklahoma, Indiana, South Dakota, North Dakota, New Mexico, and Kentucky have the greatest economic potential.

The economic potential of behind-the-meter wind applications in 2022. Texas, Minnesota, Montana, Colorado, Oklahoma, Indiana, South Dakota, North Dakota, New Mexico, and Kentucky have the greatest economic potential.NREL also found that the regions with the highest potential for distributed wind tend to have a combination of high-quality wind, relatively high electricity rates for behind-the-meter applications, higher wholesale power rates for front-of-the-meter applications, and siting availability.

The Midwest and Heartland regions overall had the highest potential for distributed wind, and the Pacific and Northeast regions had significant potential for expansion of behind-the-meter distributed wind deployments.

As modeled, agricultural land was found to have the highest distributed wind potential. But residential, commercial, and industrial land also were found to have gigawatt-scale potential, particularly for behind-the-meter applications.

NREL found that states with the most near-term potential for behind-the-meter applications included Texas, Minnesota, Montana, Colorado, Oklahoma, and Indiana. States with the most near-term potential for front-of-the-meter applications included Oklahoma, Nebraska, Illinois, Kansas, Iowa, and South Dakota.

States across much of the Northeast as well as California were found to have lower quantities of profitable distributed wind potential, but select locations with significant wind resources existed, which, when combined with generally higher retail electricity rates in these regions, could offer development opportunities.